NOW YOU CAN KNOW… How Much Your Investor is Losing by Foreclosing on Your Home.

What if you could know the answer to that question? Well, if your loan is in a securitized REMIC trust… FOR THE FIRST TIME… you can… read on.

You couldn’t keep up on your mortgage payments. Maybe they went up, maybe your income went down, or maybe it was both things happening at once, but whatever the cause, the point is that you fell behind… or knew you would have eventually… so you applied for a loan modification.

Now you’re told that the decision to modify your loan or foreclose on your home depends on whether the investor that owns your loan will come out ahead financially by modifying it… or foreclosing and selling it to someone else.

That’s what the NPV test is supposed to determine, whether the investor who put up the money for your loan will make more money by foreclosing and re-selling, or whether it makes more sense financially to modify your loan so you can continue to make the payments. Sure, modifying your loan will mean you’ll pay less than you were supposed to pay, in most cases, but if the amount you’ll pay with a modified loan is more than the investor would get by re-selling your home, wouldn’t it be better for the investor to modify? Of course it would.

Isn’t that what this foreclosure crisis is all about… whether it’s in the best interests of the investor to foreclose or modify the loan? When the investor comes out ahead by modifying, the servicer is supposed to modify. And when the opposite is true, they should foreclose. Right? Of course, that’s right.

And I guarantee you that’s what most Americans believe is happening… servicers are foreclosing when it’s in the best interests of the investors, and they’re modifying the loan when that’s not the case.

But the NPV test is only a forecast of whether the investor will make more money modifying than foreclosing… it’s a formula that provides a “best guess” at how things will work out financially for the investor in the future if your loan is modified today. It doesn’t actually show what will happen in the future because no one can know what the future will bring. All we can do is create a formula that provides a forecast… an estimate… a best guess, if you will… and that’s what the NPV test is designed to do.

NPV stands for Net Present Value, and it’s a calculation that every first year business school student is taught in finance and accounting class. It calculates the present value of a future amount… some people think of it as the time value of money. But, no matter what… it’s forecasting the future, so it could come true… and it might not.

However, once the trust that holds your loan and others has been around for several years, a number of loans have defaulted, been foreclosed on and re-sold, and a number have pre-paid, which is usually done by refinancing. Once the trust has had experience with those sort of events, we don’t need to rely only an NPV forecast anymore to see how much is lost when a loan is liquidated through foreclosure … we can look at the ACTUAL losses that have accrued to the trust when foreclosing on homes… and we can see exactly how much the investor lost. And then we can compare those losses to the financial outcomes of modified loans.

Okay, so now we just have to take a few minutes to make sure we understand what causes investors, or more accurately the trusts that hold the loans, to lose money. Then I’ll show you how we might use knowledge of investor losses to help save homes.

There are many costs that a trust must pay over the years, but the two most significant events that can change what an investor earns result from loan defaults and loan prepayments.

Prepayment Risk…

Prepayment risk most often refers to loans being refinanced, although it can also refer to loans that are paid off early with funds provided by the borrower.

Up until this last financial crisis, the biggest threat to investors in mortgage-backed securities was pre-payment risk, because when a loan is refinanced, it is paid off by the new loan and although that does mean that the investors receive their principal back, they stop receiving interest on that principal amount and they’re left to reinvest their capital somewhere else in order to continue earning a return on their money. That’s easy to see, right?

The thing is that when loans refinance it generally means that interest rates have gone down, because that’s when people refinance… when they can take advantage of the lower rates that have become available since their loan was originated. When interest rates go up, almost no one refinances, because to do so would mean having to pay a higher rate than was available when they got their loan.

So, when interest rates go down, and people refinance, the investors are forced to reinvest their capital, but now they have to do so at lower rates than they were earning before rates dropped. And that’s what is known as the “prepayment risk” associated with mortgage-backed securities.

Of course, when interest rates rise, while there are fewer prepayments, there are often more loans that go into default as those with adjustable rate loans, find that they can’t keep up with the higher payments that result from their loans adjusting.

And as we’ve all seen these last few years, even if interest rates don’t go up, should home values fall and the economy go into a recession, causing unemployment to rise, median incomes to fall and/or should the availability of credit tighten… any or all of those things can lead to increasing numbers of defaulting loans.

When a loan defaults, the investor stops receiving the monthly payments of principal and interest, and after a certain number of months, moves to take back the property so it can be re-sold and the proceeds returned to the investor… minus the costs of foreclosing and whatever losses have occurred.

Loss Severity… Today’s 800 Pound Gorilla in the Room.

The term used to describe the losses that investors take when foreclosing and reselling a home is “loss severity.” It answers the question: How severe was the loss that resulted from foreclosing and then reselling the home.

In past years, with home prices steadily rising, sometimes by the time a loan was foreclosed on and resold, the price of that home had increased, so the investor actually received more from the sale than he or she had invested. When that happened, perhaps the excess received covered the costs associated with the foreclosure and sale, so the investor was actually made whole. But since the financial crisis and meltdown of the mortgage and housing markets, home values have fallen so that certainly hasn’t happened often, if at all.

When home prices are declining or staying flat, investors want to foreclose as quickly as possible so they can resell the home before prices fall any further. But that hasn’t been happening these last five years either. In fact, today it’s not uncommon to find homeowners still living in their homes even though they haven’t made their payments in three… four… or even five or more years.

In some states, like New York as one example, it takes an average of more than 1,000 days to foreclose on a home, and that doesn’t include how long the home may have to sit on the market before it sells… in California, on the other hand, it takes something approaching 600 days to foreclose, before you can sell the home at a trustee sale or list it for sale as an REO.

From the time a borrower stops making his or her payments, to the time the home is reposed and sold, the investor is losing money. Not only is the investor losing the interest payments he or she would receive if the payments were being made, but in addition, the investor is also paying the property taxes and may also have to pay association dues to prevent the homeowner’s association from forcing the sale of the home.

Then there’s the question of damage to the home that the investor must pay to bring the home back up to code before selling it. Not everyone is happy about losing a home to foreclosure, and well… let’s just say damage happens, and leave it at that.

Additionally, the longer a home sits empty, the more maintenance it requires, and in some parts of the country, where winters are harsh or summers are sweltering, homes that sit empty too long can deteriorate significantly and cost the investor a lot of money to repair.

There are other costs associated with foreclosure as well, such as legal bills and servicing fees, among others, but when you total everything up and deduct the total amount from the sales proceeds after the home is sold to a new owner… the amount at the bottom-line is called “loss severity,” and it can be expressed as either a dollar amount or as a percentage of the loan amount.

So, if the loss severity is 50 percent, and the amount of the loan is $100,000, then the total loss to the investor associated with the foreclosure and sale is $50,000.

It shouldn’t be hard to imagine that these days loss severity has to be running significantly higher than usual… maybe even higher than at any time in our nation’s history, but that doesn’t answer the question of specific losses in dollars and cents.

To do that we have to be able to look inside the trust that holds the loans and see what it has reported in terms of loss severity since its inception. And that’s precisely what you can now do… with an RMBS Trust Liquidation Analysis Report, which you can now order through Mandelman Matters… but I’ll get back to that in a moment.

Now that’s what I call loss severity…

Looking at the Actual Loss Severities Reported by RMBS Trusts Today…

I’ve always known, anecdotally at least, that loss severities today had to be high… very high, even. But I didn’t know the exact numbers associated with any given trust or loan amount. But, the other day, when I ran an RMBS Trust Liquidation Analysis Report on a specific trust, I saw what the numbers and percentages were… and I have to tell you that even I was somewhat shocked at what I saw.

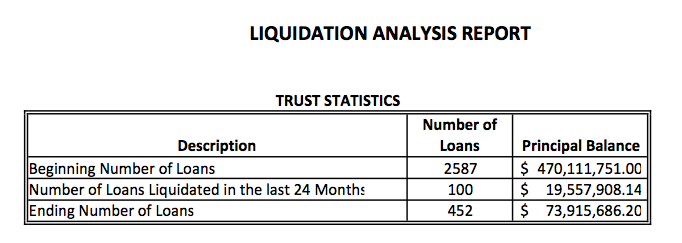

The trust being looked at, as you can see in the Liquidation Analysis chart below, started out with 2587 loans in it, but today there are only 452 loans remaining after defaults and prepayments. Over the last 24 months, 100 loans in this trust have been liquidated, meaning the homes were foreclosed on, and sold either at auction or after having been listed for sale as an REO property by the servicers.

When the trust was first formed, the total dollar value of the loans in the trust was $470 million and change, and today the remaining loans are valued at just over $73 million. The 100 loans that were liquidated during the last two years cost the trust almost $20 million.

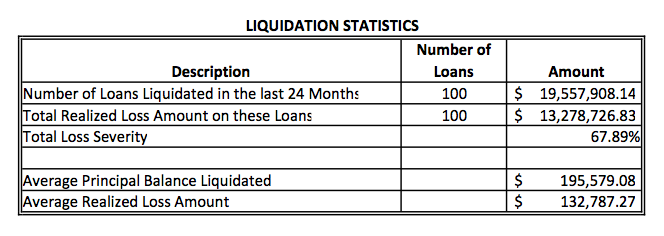

The next chart shown below shows you the total realized loss amount from the loans that were liquidated, and just below that amount, which you can see in the second line down was just over $13 million, you see the average loss severity, expressed in percentage terms… 67.89%.

That means that on average, when this trust forecloses on a home and resells it, the trust realizes a loss of almost 70% of the loan value. But let’s keep going because we want to get more specific than that… we want to know how much would have been were our loan to be liquidated by this trust through foreclosure.

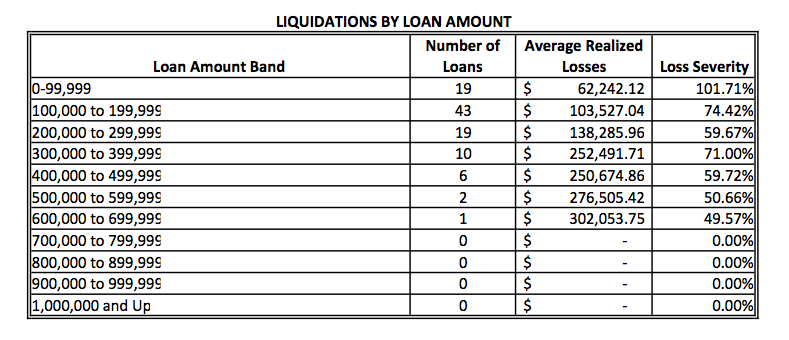

So, the next chart shows liquidations by loan amount, and for convenience sake, the loan amounts have been compiled into bands, $0 – $99,999… $100,000 – $199,000… $200,000 – $299,999… $300,000 – $399,000 and so forth, all the way up to $699,999, because this trust doesn’t have any loans over $700,000.

The next column over from the left shows the number of loans that have been liquidated in each banded loan amount, for example, there have been 19 loans under $100,000 liquidated by this trust during the last 24 months. And the next column over shows the dollar amount of the average realized loss for each of those 19 liquidated loans… $62,242.12… with the last column showing us that the loss severity for those 19 loans was 101.71%.

Or, in other words, this trust lost more than 100% of the loan balances when it foreclosed on homes under $100,000.

It sure seems like if those loans for $100,000 and under had been modified, the investors would have had to come out ahead of losing everything and then some, as they did by foreclosing, wouldn’t you think? Don’t answer that, I’m being sarcastic… of course the investors should have modified those loans… anything is better than losing everything.

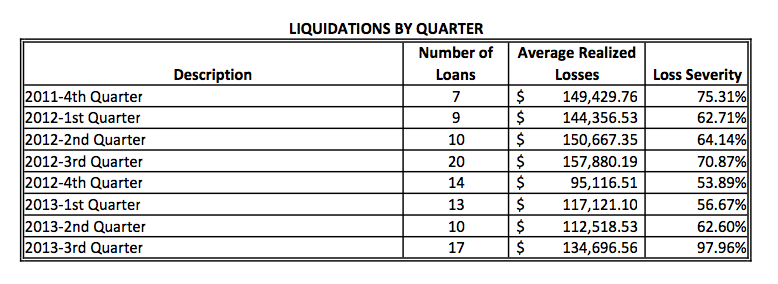

Next, we can look at the losses by quarter to see if we’re losing more or less as time passes, and in the chart below, you’ll see the opposite is true. For the 4th quarter of 2011, loss severity for this trust was roughly 75%, and for the 3rd quarter of 2013, loss severity jumped up to a little over 97%.

Now, I don’t want to get too technical and lose anyone, but there would be other things broken down and reported as well, like the amounts due in terms of unpaid principal, the amounts of accrued interest, and a category for miscellaneous expenses associated with foreclosing and selling the homes.

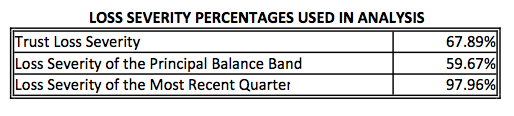

But, after factoring those sorts of things into the calculation, we’re left with looking at how much was lost on one $320,475.57 loan. And there are three different loss severity percentages we might want to consider…

- Trust Loss Severity – The average percentage loss on foreclosures for the trust overall.

- The loss severity for the principal balance band, meaning by the price band of the loan.

- Loss severity for the most recent quarter, which is the third quarter of 2013 in this example.

So, in the chart below, you’ll find each one of those measurements of loss severity shown… the overall trust loss severity is 67.89%, for the principal balance band it’s 59.67%… and the latest quarter, as we saw above, it’s 97.96%… almost 100% losses from foreclosing as of the third quarter of this year. Things seem to be getting worse as time goes by, which should come as no surprise.

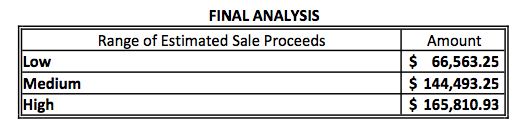

Finally, we might want to know how much the trust is expecting to get out of a loan liquidated today, and so we’d want to apply all three loss severity percentages to the specific loan’s balance and the result would be a low, medium and high amount that the trust can expect to realize.

As you can see in the chart above, the most this trust can expect to realize by liquidating a $320,475.57 loan based on its own data for the last two years is $165,810.93. The worst case scenario is $66,563.25.

So, should this trust modify that $320k loan, or should it foreclose and sell the property? Well, to be fair… that depends on one thing I haven’t mentioned yet… the probability of the borrower re-defaulting in the future after the loan has been modified, because obviously the cost of defaults and foreclosing is high… so most certainly the trust doesn’t want to have to go through it twice on one loan or its loss severity could climb towards 200% in some cases, right? That’s correct.

But, should that trust agree to short sale that home for something around $165k? Well, that depends on the market value of the property too. Obviously, if the home were to appraise for $250,000, it wouldn’t make sense to take $165k and forget about the market price, but if the home has been in inventory for some time, perhaps there are times when accepting $165k might look pretty darn good.

And regardless, doesn’t it make negotiating a short sale or modification more closely tied to the actual financial performance of the specific trust that owns the loan? Instead of working in the dark and being asked to guess a number between one and 10… and you saying “7” and them responding by saying, “Wrong, try again?”

I’ll tell you this… if I were heading into mediation, or trying to get my own loan modified, I’d definitely want to know what the trust that owns my loan is expecting to lose by foreclosing as opposed to modifying my loan, especially if the trust is expecting to lose 70 percent or more.

I think the entire country is under the impression that servicers foreclose because it’s in the best financial interests of the investors, and perhaps sometimes they do… but data from this trust and others I’ve looked at, to my way of thinking, proves that’s not always the case. And no homeowner has ever been able to prove that before now.

Now homeowners and Realtors can know the loss severity being experienced by the specific trust that holds a specific loan and I have to think having this knowledge, whether in mediation or when trying to get a loan modified will prove to be an advantage in many instances.

The RMBS Trust Liquidation Analysis Report is not available for loans owned by Fannie Mae or Freddie Mac… yet… but it is available for loans securitized by Wall Street… and that’s still a whole lot of delinquent loans.

So, if your loan was securitized by Wall Street and is held in a REMIC trust, you can get this report right now, by simply sending an email to Mandelman Matters at… Mandelman@mac.com

… and PLEASE type the SUBJECT in ALL CAPS…

I’M INTERESTED IN THE LIQUIDATION ANALYSIS REPORT

Then in the message, please provide your contact information and when would be a good time for me to call so we can discuss the report further and I can answer any questions you might have.

And you may be assured that the information you receive in the Liquidation Analysis Report is rock-solid correct… it’s reported by Master Servicers to trustees as of the last day of the prior month and it’s delivered by the structured finance industry standard in trust intelligence and surveillance. It’s the same data used to value trust assets by investors all over the world and expert witness testimony is available should you need to bring the data in the courtroom.

I don’t know how homeowners having this information will impact their mediation or loan modification processes… no one does because homeowners have never had access to this kind of information before now.

But I have to think it will help, and perhaps it will lead to turning this crisis on its ear as homeowners are finally able to prove that foreclosures are not always happening because they are in the best financial interests of investors.

And when you order your report, you also get me… and Mandelman Matters… because I’ll write about whatever happens as a result of you using this information to get your loan modified.

It’s time to shake things up a bit, don’t you think?

Order your Liquidation Analysis Report today by sending an email to me today at Mandelman@mac.com. And please don’t worry… although it can’t be free because it does cost money to get the data… it’s also not expensive.

Mandelman out.