GAO REPORT SAYS IT AGAIN: Treasury NEEDS to improve HAMP Data Analysis

The Government Accountability Office, or GAO, released a report on October 6, 2014, that seems to have gone largely unnoticed, not that I’m the least bit surprised about that. The report, which you’ll find in its entirety below, recommends that the Treasury Department improve its capabilities and methodologies related to analyzing the data it collects on HAMP, the Home Affordable Modification Program that has consistently been producing underwhelming results since its inception in 2009.

Lest we all forget, the amount we originally allocated to the HAMP program was $75 billion. After we saw that it wasn’t working all that well, we reduced the amount allocated to $50 billion, and later we reduced it again to $38.5 billion. And still, as of today, we’ve only spent about a third of that amount on HAMP, with far fewer borrowers receiving loan modifications under HAMP than Treasury originally estimated.

I have to say that I think it’s the only government program I’ve ever heard of that continually costs less than it was supposed to cost… does less than it was supposed to do… and yet is still widely heralded as “a success,” as opposed to being seen as clearly in need of ongoing improvement.

Reading the report, which you can do below, is reminiscent of Stanley Kubrick’s brilliant satire, “Dr. Strangelove – Or: How I learned to stop worrying and Love the Bomb.”

The report, whose first headline reads: Treasury Could Better Analyze Data to Improve Oversight of Servicers’ Practices, runs 55 pages in total length, but you get a feel for things starting on page one when it begins as follows…

“… the number of new borrowers added to the Home Affordable Modification Program (HAMP), the key component of the Making Home Affordable (MHA) program, began to decline in late 2013 after remaining relatively steady since 2012.

Treasury has taken steps to assist more homeowners and also to address upcoming interest rate increases for borrowers already in the program (after 5 years, interest rates on modified loans may gradually increase to the market rate at the time of the modification). For example, Treasury has extended the HAMP deadline for a third time to at least December 31, 2016, and required servicers to inform borrowers about upcoming interest rate changes.”

(“Steady since 2012, but started to decline in late 2013?” Okay, let’s just let that one go, shall we… I’m certainly not here to pick nits, as some might say.)

So, if you’ll just follow me on this, that paragraph is saying that based on the decline in modifications that began in late 2013, Treasury took steps to assist more borrowers… that sounds good at least… and to address the upcoming interest rate increases that would be coming for those modified in 2009. And that also sounds like something worth doing.

Assist more borrowers and address the rising rates about to hit those who received modifications that optimistically only offered to lower rates for five years… okay, I’m in complete agreement with both of those things as being good things to do.

Okay, so what did Treasury do exactly to assist more borrowers, and address the coming of rising rates? Well, it tells you right there in the last sentence of that first paragraph of the GAO report, where it says…

“For example, Treasury has extended the HAMP deadline for a third time to at least December 31, 2016, and required servicers to inform borrowers about upcoming interest rate changes.”

That’s what the United States Treasury Department did to assist more borrowers and address the coming of rising rates? They extended the deadline for the at least somewhat dysfunctional program… and required servicers to notify borrowers when their rates would be going up?

We needed the United States Treasury Department to do those two things? Extend a deadline that obviously needed to be extended because it wasn’t working to solve the underlying problem, and then to tell servicers they have to tell borrowers when their payments are about to rise?

Do servicers really need to be told that they have to tell borrowers when their mortgage payments are about to rise by hundreds of dollars a month? Wouldn’t servicers just think to do that as a matter of course… like because it’s simply a good business practice to let people know about something like that… if for no other reason than to reduce the number of phone calls received from borrowers once they received their higher bills in the mail?

And how much effort was actually needed at Treasury to extend the deadline that everyone in the country paying any attention at all knew would need to be extended four years ago? Isn’t that sort of a phone-it-in sort of thing for the Treasury Department?

“Okay, Margaret… go ahead and announce we’re extending the date to the end of 2016.”

“Roger that, Sir. I’ll take care of it as soon as I get back from lunch.”

Okay, so I’m one paragraph deep into the 55-page GAO report, and I’m positively nonplussed, at best. At worst, I’m thinking about running out my front door and directly into oncoming traffic.

Then we move onto the data collection and analysis discussion, which is the meat of the GAO recommendation after all, and it says the following…

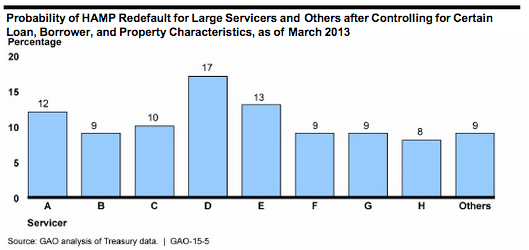

“Treasury monitors HAMP denial and re-default rates, but its evaluation of data to help explain the reasons for differences among servicers is limited. GAO’s analysis of HAMP data found wide variation among servicers in reasons for denials of trial modifications. Some of these variations may be due to differences in servicer practices that would not necessarily be identified by Treasury’s compliance review process or analysis for reporting errors.

GAO also identified wide variations in the probability of re-default even after controlling for differences in servicers’ loan, borrower, and property characteristics, using available data (see chart below).

Federal internal control standards state that analyzing relationships among data helps inform control and performance monitoring activities. Without more fully evaluating servicer data, Treasury may miss opportunities to identify and address servicer weaknesses and assist and retain as many borrowers as possible.”

I don’t know why, but I feel compelled to point out that we’re talking about a program that was rolled out in 2009… it’ll be SIX YEARS AGO in just a few months. And I’m being told that after almost six years, the ability of the United States Treasury Department to explain why different servicers experience different outcomes related to the federal program is… LIMITED?

I don’t know who wrote the GAO report, there’s no name on it, but to that person I’d very much like to ask the following question: “Limited by who or what, jackass?”

Who or what exactly is constraining the capabilities of the United States Treasury Department? Because whoever is doing it should be brought up on charges of treason, right? And whatever is causing it (assuming it’s a “what,” as opposed to a “who”) I’d say should be removed immediately.

I simply don’t need there to be any sort of unidentifiable or unnamed force out there capable of constraining the United States Treasury Department’s capabilities under any circumstances, and frankly, sentences that lead me to believe otherwise make me reticent to pay my taxes.

In a nutshell, what I’m trying to say is… who on God’s green Earth is running this show?

I’m asking because as I read the paragraphs above, it strikes me that after overseeing the $38.5 billion taxpayer funded program, the Treasury Department possesses almost no idea what servicers are doing as related to granting loan modifications.

It would seem that they have no idea what is causing re-defaults at one servicer as opposed to re-defaults at another… no idea why borrowers are denied at one as opposed to another… no idea whether servicers are in compliance with much of anything… and based on any of those conclusions, obviously no clue as to what even needs to be fixed or even improved about the program.

As related to servicers specifically having controls in place to comply with fair lending laws, something the Treasury Department itself required of servicers, the report explains at the bottom of page one that Treasury has declined to monitor or assess these controls because, they say, there are others agencies for that.

In response to this gibberish, the GAO report states…

“Without such assessments, Treasury cannot determine whether servicers are complying with Treasury’s requirement.”

It reminds me of a sentence I wrote several years ago that I’ve never been able to get out of my mind. It was in an article that I wrote about in August of 2010, under the headline, “It’s a Matter of Principal – HAMP’s New PRA.” The sentence I’m reminded of was in reference to Fannie and Freddie choosing not to participate in the government program known as the “Principal Reduction Alternative,” or PRA, and to communicate this piece of news, I penned the sentence…

“Of course, the GSEs or Government Sponsored Entities, Fannie Mae and Freddie Mac, will not be participating in the government program.”

As I realized at the time, it’s the sort of sentence that I’m pretty sure can literally cause permanent brain damage in writers who don’t drink enough alcohol to make such memories go away… and obviously, I’m still working on that. (Actually, hang on a sec, if you wouldn’t mind… I’m just going to run into the kitchen for a glass of bourbon… be right back.)

Ahhh… okay, I’ll try to wrap this whole commentary up for everyone’s sake, since I fully realize that it has no real potential to make a point… or at least it won’t point out anything that anyone will even try to do something about… so what’s the point, right?

So, before I leave it to the reader whether or not to read the GOA report below and decide for himself or herself whether anything should be said to his or her elected representatives, I thought it would be worth taking a look at what the report says under the heading: “Why the GAO Did This Study.” It says…

“Treasury introduced MHA in early 2009and has allocated $38.5 billion in TARP funds to help struggling homeowners avoid potential foreclosure. The Emergency Economic Stabilization Act of 2008 requires GAO to report every 60 days on TARP activities.

This 60-day report examines (1) the status of TARP-funded housing programs, (2) Treasury’s efforts to monitor and evaluate HAMP denial and re-default rates among servicers, and (3) the status of the implementation of GAO’s prior recommendations related to TARP-funded housing programs. To do this work, GAO reviewed program documentation, analyzed HAMP loan-level data, and interviewed knowledgeable Treasury officials.”

Okay, so at least I now understand why the GAO did its report in the first place. It’s because “The Emergency Economic Stabilization Act of 2008 requires GAO to report every 60 days on TARP activities.” That makes total sense for the GAO, but it does make me wonder what’s my excuse for commenting on it?

I’m almost positive that I’m not even mentioned in the Emergency Economic Stabilization Act of 2008.

As to the other stated purposes, I’ve been trying to avoid having to say anything about it since I started typing this excursion in to the world of Dr. Strangelove. It’s because I’ve written about this exact sort of inconceivable nonsense going on at Treasury related to HAMP data before, and not just once but multiple times. In fact, I’ve written about it every time it’s been thrown in my face by one report or another that talked about HAMP re-default and approval rates over the last six years.

Here’s what I said at the end of my last piece about this same topic…

So, are we anywhere close to stopping the charade? Or need we continue to act as if we’re entirely unsure of what’s going on all around us… and has been going on for the last six years straight, as we continue to pretend that stimulus is recovery and that real estate is coming back.

HAMP is a government program, right? I know it’s a government program because no one in the private sector would ever come up with such a wonky acronym or dysfunctional mess. So, if it’s a government program, perhaps the government could actually step into it a bit and take a look at what goes on with it when people apply for a loan modification.

Maybe you could get the CIA to weigh in on how you could secret shop Wells Fargo… that’d be illuminating, I can assure you of that.

Or, how about this… every time it’s determined by a court in this country that a homeowner was seriously mistreated in the loan modification process, the servicer’s CEO, the Treasury Secretary and Ed DeMarco have to go pick up trash on the freeway wearing orange vests for the weekend. I bet that would modify some servicer behaviors in a damn hurry.

I’m sure that at the very least you wouldn’t be asking Treasury every six months to investigate something that Treasury CLEARLY DOES NOT WANT TO INVESTIGATE. If they did, they probably would have found time to do so during the past SIX YEARS, don’t you think?

(A NOTE TO THE READER: My last piece on this subject was titled: “Re-Default Redoux… The Debate Over Loan Mods is as Stupid as Ever,” and it was really worth reading, in my opinion, although relatively few did and I think it had something to do with my headline not being search engine optimized… or friendly… or whatever. You should try it, however, because unfortunately it’s still every bit as relevant as it was when written, and it’s got several funny parts… I laughed anyway. And if not, heck, I don’t blame you. I do understand simply not wanting to know.)

So, once again, what the GAO recommends in its most recent report is…

GAO recommends that Treasury conduct periodic evaluations to help explain differences among MHA servicers (1) in the reasons they gave for denying applications for HAMP trial modifications and (2) in HAMP loan modification re-default rates.

Such evaluations would help inform compliance reviews of individual servicers and help identify any needed program policy changes.

Look, clearly Treasury doesn’t want to know about any of those things.

They don’t want to know about differences between servicers when it comes to modifying loans under HAMP or otherwise. They don’t want to know why people are denied for trial modifications, and they sure as heck don’t want to know anything about re-default rates.

Do you want to how I can be so rock solid certain that the Treasury Department does not want to know about these things? I mean, one obvious reason is that if they did, then over the last six years they would have figured out how to know right down to the penny or minute detail.

And if you’re not sure I’m right about that, they I would encourage you to click the link that follows that will take you to a report on the U.S. Treasury’s website titled: “U.S. International Reserve Position,” on which you’ll find the data to explain why “U.S. reserve assets (and other foreign currency assets) totaled $137,772 million as of the end of that week, compared to $137,034 million as of the end of the prior week.”

Or, if that doesn’t sway you, then try this link to the Treasury Direct Report titled: “The Debt to the Penny and Who Holds It,” which tracks “the data on total public debt outstanding daily from 01/04/1993 through 10/15/2014. The debt held by the public versus intragovernmental holdings data is available:

- Yearly (on a fiscal basis) from 09/30/1997 through 09/30/2001.

- Monthly from 09/30/2001 through 03/31/2005

- Daily from 03/31/2005 through 10/15/2014

Best I can tell, that report is somehow managing to track combined debt of roughly $17 trillion dollars… TO THE PENNY… and not only is it available to review on a yearly, monthly, or daily basis, but you can download the report in Excel, XML, CSV, TSV, HTML, JSON or PDF.

But, as to why Wells Fargo almost NEVER modifies loans held in Wells Fargo securitized trusts, even though the applicable PSAs don’t prohibit loan modifications… or what might be causing re-defaults of some modifications but not others, or at some servicers and not others… or even why some servicers modify many more loans than do others…

… Well, I’m sorry, boys and girls in Never-Never Land… the United State Department of the Treasury can’t help you with any of that, because after six years, its ability to explain why different servicers experience different outcomes is… LIMITED.

So, since Treasury has LIMITED ability in that regard, try asking them an easier question like who specifically, whether a member of the public or an intragovernmental holder, owns TO THE PENNY roughly $17 trillion in U.S. debt… as of the last Thursday in March, 2013. That they can answer accurately… and literally… in a matter of seconds.

Does everyone have it straight by now? Can I stop caring about, or at least writing about this topic forever and ever, amen? From your lips to God’s ears… let it be so. Someone else is going to have to take this one from here, because I have seen enough.

As in… ball four, take a hike, the showers are on and I’m all done here.

But lastly, at least for my purposes, it also says…

“The GAO hopes more robust data analysis will help Treasury increase oversight and transparency, improve its policies and guidance, and ensure that HAMP reaches the greatest number of eligible borrowers.”

Well, there’s certainly more than enough HOPING going around these days. In fact, we seem to be positively awash with HOPE in this country. HOPE, HOPE, HOPE.

Honestly, I’m starting to lose my ability to HOPE that there’s still HOPE.

Mandelman out.

~~~

Gao Report (Oct 2014) Troubled Asset Relief Program